Five Key Areas to be Addressed by the Anti-Avoidance Tax Directive Adopted on 12 July 2016     On 12 July 2016, the EU’s Economic and Financial Affairs Council (ECOFIN) formally adopted the Anti-Tax Avoidance Directive (ATAD) and it was subsequently published in the Official Journal of the European Union on 19 July 2016. This represents unanimous agreement from 28 countries on a set of five minimum implementing measures to tackle aggressive tax planning and other corporate tax avoidance strategies. For non-tax specialists and the public at large, these are esoteric adjustments that are difficult to interpret. However, the fiscal impact will affect everyone in the EU. The Directive attempts to address some of the most egregious international tax loopholes, while allowing individual EU countries to go further at national level, if they wish.

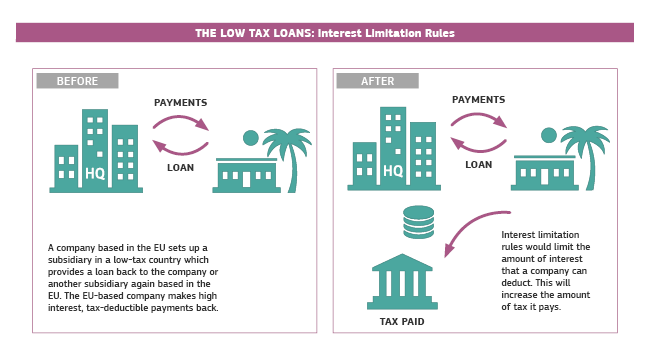

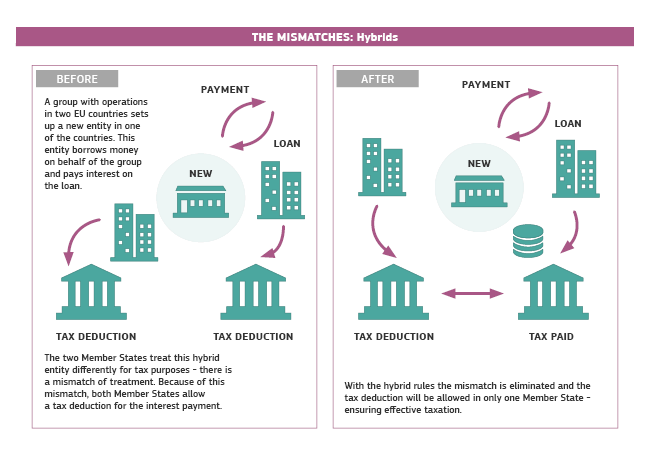

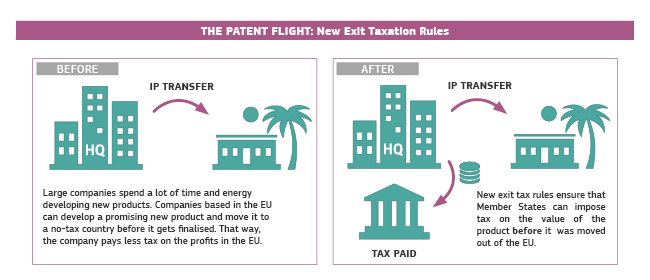

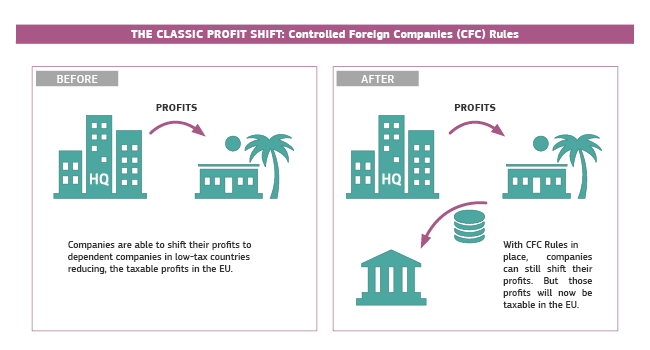

Hybrid mismatches (double interest deductions, etc) are tackled by the Directive. However, the provision only applies to hybrid mismatches within the EU. The number of situations where an EU entity would give rise to a hybrid mismatch benefit appears to be small and this type of mismatch would be subject to pre-existing EU control measures such as those contained in the EU Parent Subsidiary Directive. The ECOFIN has requested the European Commission to put forward a proposal relating to hybrid mismatches with non-EU countries by October 2016. New limitations on interest deductions may be deferred until as far away as 2024 for countries that already have strong targeted rules, and the EU Commission will determine which countries qualify for this type of deferred implementation. It seems likely that Ireland and Luxembourg will meet the criteria. The Netherlands also plans to tighten its own interest limitation rules before end-2016. Financial undertakings (financial institutions, insurance undertakings, UCITS, AIFs, etc) are temporarily excluded from the provisions of the Directive. The bulk of the Anti-Tax Avoidance Directive will be in effect by the start of 2019, while the exit tax must apply from 2020. The Directive also contains grandfathering provisions for certain transactions already in place before June 2016. Some countries, such as the UK, will fast-track implementation as well as applying tighter unilateral controls. While the Directive will probably not have an enormous financial impact in the short-term, it is a truly momentous, if not revolutionary, first step from the EU in implementing the findings from the OECD’s BEPS project. The five key areas addressed by the Directive are summarised briefly below: 1. Hybrid mismatches This provision tackles cross-border arrangements that result in either (i) a double deduction or (ii) a deduction without inclusion by the other EU country. 2 Interest deductibility limitation The essence of the new rule is that excess borrowing costs will be deductible up to 30% of the company’s EBITDA or, optionally, up to a EUR 3m threshold. A grandfathering provision applies to loans concluded before 17 June 2016. As mentioned above, the new limitations on interest deductions may be deferred until 2024 for countries that already have strong targeted rules. Ultimately, the EU taxation impact of these interest limitation provisions should be substantial. 3. Exit taxation An exit tax will be applied to certain cross-border transfers of assets or residence within the EU or to a third country. For transfers within EU or EEA countries, the rule includes a tax deferral mechanism that allows companies to pay the tax in instalments over five years. Ireland, for example, already applies a broadly similar type of exit tax. 4. General Anti-Abuse Rule (GAAR) The GAAR is similar to that inserted in the EU Parent-Subsidiary Directive and tackles artificial tax arrangements (i.e. not based on valid commercial or economic reasons) where no other specific anti-avoidance rule applies; 5. Controlled Foreign Company (CFC) rule A CFC rule will apply if the corporate income tax paid by the CFC is lower than 40% of the tax that it would have been charged in the home/controlling jurisdiction. Under one of two implementation options, there is a carve-out for companies with substantive economic activity (staff, premises, equipment, assets, risk undertaken) and this is the route that Ireland will likely take as it is consistent with its longstanding inward investment strategy.

0 Comments

|

AuthorKieran Desmond

Archives

December 2017

Categories

All

|

RSS Feed

RSS Feed